PrimeKey Analysis consolidates key property attributes into one clear, objective score, providing a structured, data-driven way to evaluate any Singapore property, so you can move beyond guesswork, uncover hidden risks, understand real demand strength, and assess exit potential before committing hundreds of thousands with confidence.

Too many projects, too many opinions, and every agent says their unit is “the best buy”. Looking only at PSF and recent transactions doesn’t answer the most important question:

PrimeKey Analysis is a structured way to cut through marketing noise using real market data and forward-looking indicators. It evaluates each property based on its risk versus reward potential, not on hype or showroom excitement.

With PrimeKey, you don’t just buy a home. You buy a future outcome you understand.

PrimeKey Analysis combines data-driven metrics with deep market experience to sieve and grade assets objectively. This helps buyers and investors identify genuine opportunities, avoid blind spots, and make decisions grounded in logic rather than emotion.

The result is a clearer, more confident approach to choosing properties with real staying power, whether for own stay or long-term growth.

These are the core factors used to evaluate properties in Singapore. (Not every factor carries the same weight — I adjust based on your goal.)

Walking distance to train stations directly impacts livability, rental demand and widens the audience profiles - Typically the more convenient it is, the more desired it is.

Being located within a URA Masterplan growth hotspot historically delivers higher price growth over other estates.

Future releases of lands nearby fuel future growth, as land prices escalates over time historically - lifting asset values.

Larger developments enjoy lower density living, higher variety of facilities and higher resale volume, reducing liquidity risks.

99-years leasehold properties typically go through a 3 stage life cycle - Growth, stagnation and declination. A healthy remaining tenure helps prevent equity decay and higher probability of a profitable exit.

Higher yields indicate strong demand, providing better cash flow for landlords and increased demand from potential investors.

Being within 1km to a primary school helps in enrolment probabilities for families with young kids and provides a consistent demand pool.

Neighbourhoods with higher numbers of HDB flats reaching their minimum occupation period (MOP) dates generate natural demand as home owners are generally younger with stronger aspirational needs.

No single factor determines whether a Singapore property is a good purchase or investment. Strong long-term performance is usually the result of several fundamentals working together, location, demand drivers, tenure, supply outlook and buyer profile reinforcing one another.

When multiple PrimeKey pillars align, demand becomes broader and more resilient, downside risk is reduced, and price growth is more likely to remain steady across market cycles. This holistic approach helps buyers look beyond short-term trends and focus on assets with genuine staying power.

PrimeKey Analysis brings these critical factors into one clear, objective score, replacing guesswork with structured and confident decision-making for anyone buying a home or investing in property in Singapore.

Own stay • investment • upgrade • asset progression

I run PrimeKey on your choices (and alternatives) to highlight blind spots and strengths.

We decide how to enter safely, and how to exit with a realistic buyer pool in mind.

Share the project or unit you’re looking at — I’ll show you strengths, blind spots and better alternatives if any.

Share what you’re considering. I’ll reply with a data-backed view and what to watch out for.

By submitting, you agree to be contacted for this request. Your details won’t be shared.

Walking distance to an MRT station is one of the most influential factors for both rental demand and resale performance in Singapore. Properties that are genuinely within a comfortable 5–10 minute walk tend to attract a larger pool of tenants and buyers, while homes that require a bus connection or a long outdoor walk often experience slower take-up, especially in our hot and humid climate.

This preference is supported by local research. A Straits Times survey found that many residents feel owning a car becomes less necessary when public transport is within a 10-minute walk

👉 https://www.straitstimes.com/singapore/transport/less-need-to-have-car-if-its-a-10min-walk-to-public-transport

To translate walking time into distance, studies on average walking speed show that Singaporeans cover about 19 metres in 10.55 seconds, which works out to roughly 1.1km in 10 minutes

👉 www.richardwiseman.com/quirkology/pace_home.htm

This explains why the 1km radius is often used as a practical gauge of “true walkability.” Beyond this range, daily commuting comfort drops quickly, and buyer perception begins to shift from “walkable” to “need transport.”

From real market behaviour, closer MRT proximity typically leads to:

These advantages are particularly meaningful for families with school-going children and working professionals who rely on independent daily travel.

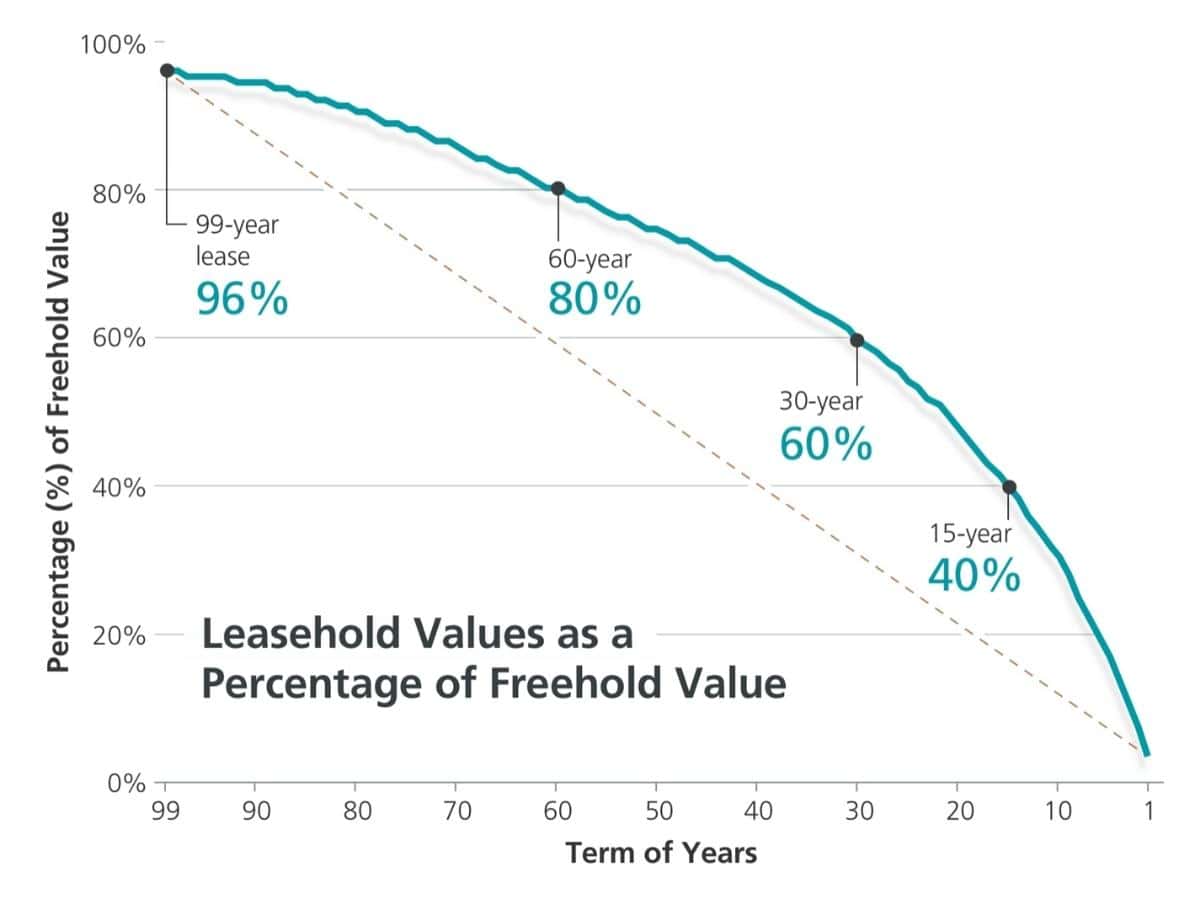

The remaining lease term directly affects long-term value, financing options, and buyer demand. Properties with a shorter balance lease generally experience slower price growth and weaker resale appeal than similar homes with a longer balance period, even when both are priced identically today.

A simple comparison illustrates this: a 99-year leasehold condo with 85 years remaining is usually more attractive to buyers and banks than one with only 55 years left. Exceptions exist, such as conservation shophouses, heritage apartments like those in Tiong Bahru, or projects with realistic en-bloc potential, but these are niche situations rather than the norm.

Government policies also play an important role. CPF usage and housing loan limits are reduced when a property’s remaining lease is not long enough to cover the buyer up to age 95. This can significantly affect affordability and buyer eligibility, especially for younger purchasers who rely on CPF and financing to enter the market.

Looking ahead, Singapore will see a growing number of 99-year leasehold condominiums from the 1980s and 1990s entering the sub-60-year range. These ageing developments may face shrinking buyer pools, as younger buyers prefer longer leases and older buyers may be cautious about committing large sums to assets with limited remaining life. Historical valuation trends, often illustrated by concepts such as Bala’s Curve referenced by the Singapore Land Authority, show that price declines tend to accelerate as leases approach their later stages.

A Short Historical Perspective

Singapore’s shift toward 99-year private developments began after the Land Acquisition Act (1966) and the Government Land Sales programme (1967), which standardised future state land to 99-year leases. During the 1970s, the modern condominium model emerged, and by the 1980s–1990s, most new private projects outside traditional freehold districts were built on 99-year tenure. This explains why many developments from that era are now approaching the critical mid-life phase of their leases.

What This Means for Buyers Today

Understanding tenure is therefore essential not only at the point of purchase, but also for planning your future exit or asset progression.

HDB upgraders are among the most consistent buyer groups in Singapore’s private property market. Regardless of market cycles, many homeowners naturally aspire to move from an HDB flat to a condominium in the same familiar neighbourhood, creating a steady, recurring source of demand.

Estates with a large number of flats reaching their Minimum Occupation Period (MOP) often experience this effect more strongly. When several BTO or resale clusters reach MOP around the same time, a wave of households begins exploring upgrade options, particularly developments close to their current schools, workplaces, and family support networks.

This buyer profile typically consists of households that have spent years building financial stability. After nearly a decade of homeownership, many are at a different stage of their careers and life goals, with growing families and stronger aspirations for lifestyle improvements. These motivations tend to persist in both rising and softer markets, making upgrader demand relatively resilient compared with purely investment-driven buying.

From a property selection perspective, locations with a healthy pipeline of MOP households often benefit from:

Understanding the surrounding upgrader ecosystem, therefore, helps buyers assess whether a project has genuine, sustainable demand beyond launch momentum.

Government Land Sales (GLS) play a powerful role in shaping price expectations within a neighbourhood. When a new site is launched and awarded at a higher land cost, it often sets a fresh benchmark for future developments. This can influence how buyers and sellers perceive the value of surrounding projects, even before the new development is completed.

Human behaviour is a key driver behind this effect. When replacement homes in the same area are priced significantly higher on a per square foot basis, owners of older projects naturally reassess their asking prices. Buyers, in turn, may view existing developments as comparatively more affordable alternatives, which can renew interest and support price movement.

Over the years, this pattern has been observed in many parts of Singapore. Areas such as Pasir Ris, Punggol, and Beauty World previously saw uplift after successive GLS launches, while more recent examples include Tampines, Tengah, and Lentor. (feel free to connect with me if you like to know more about the uplift trend of such mentioned area). As land is released in stages, rising construction costs and inflationary pressures on labour and materials often lead to progressively higher breakeven prices for each new project.

For property buyers, understanding the GLS pipeline helps to:

Looking at nearby GLS activity, therefore, provides an important forward-looking lens, rather than relying solely on past transactions.

Urban transformation plays a major role in long-term property performance. When the government invests in new transport links, business hubs, and neighbourhood amenities, demand for homes in those areas generally strengthens over time. These improvements shape where people want to live, work, and invest, thereby supporting capital appreciation.

Locations highlighted in the URA Master Plan, such as new commercial nodes, integrated transport hubs, or rejuvenation districts, have historically shown stronger price momentum compared to mature areas without major upgrades. Examples include Marina Bay, Sengkang, Jurong Lake District, Bidadari, and Beauty World, which have already experienced such growth following the announcement of the transformation. Better connectivity shortens travel time, new offices create job catchments, and fresh lifestyle amenities attract a wider resident profile. Together, these factors expand the pool of buyers and tenants.

Past trends suggest a close relationship between infrastructure investment and property growth. As new MRT lines, mixed-use developments, and employment centres come online, surrounding projects often benefit from improved liveability and rising desirability. However, not all hotspots are equal; some are large-scale regional transformations, while others are smaller neighbourhood enhancements.

For long-term buyers, focusing on major growth hotspots with sustained plans for commercial activity, residential supply, and community facilities can provide a more reliable tailwind than short-term speculation.

The number of units in a development has a meaningful impact on livability, maintenance costs, and resale performance. Larger projects typically benefit from economies of scale, enabling residents to access more comprehensive facilities and lower per-unit maintenance costs than boutique developments with only a small number of homes.

From a practical standpoint, bigger developments often offer a wider range of amenities, such as multiple pools, gyms, function rooms, and landscaped spaces, which enhance everyday living and long-term appeal to both tenants and buyers. These features can make a project more competitive in the rental market and help it stay attractive even as newer projects enter the neighbourhood.

Maintenance is another important consideration. With more owners contributing to the sinking fund and monthly management fees, larger projects can spread the cost of lifts, security systems, landscaping, and general repairs more efficiently. In smaller developments, the same expenses are shared by far fewer households, which can lead to noticeably higher fees and occasional challenges in maintaining the property to a comparable standard.

Market liquidity is also typically stronger in sizeable developments. A higher unit count usually brings:

This steady flow of activity reduces the risk of having to discount heavily during resale. While not guaranteed, larger land footprints and unit counts may also offer better prospects if collective sale opportunities arise in the future.

For these reasons, development size is a key factor when assessing both lifestyle quality and exit strategy.

Rental yield is a key indicator of real demand and financial sustainability. A healthy yield provides income support during the holding period, helping owners meet mortgage repayments and ongoing costs even when the sales market slows. This cash-flow buffer reduces the pressure to sell at an unfavourable time and gives investors greater control over their exit strategy.

Trends in rental performance also reveal a project’s underlying strength. When rents for a specific unit type begin to decline, it may signal ageing facilities, rising competition from newer developments, or a mismatch between the unit layout and the neighbourhood’s tenant profile. Understanding these patterns helps buyers avoid properties that could struggle to attract tenants in the future.

Tenant suitability varies across locations. For example, in OCR estates further from MRT stations, one-bedroom units may face weaker demand if the area is dominated by families rather than singles or expatriates. On the other hand, projects near business parks, international schools, or major employment nodes often support stronger and more stable rents.

A practical approach is to study the tenant catchment around a development, nearby offices, education institutions, medical hubs, and transport links, and match the unit mix accordingly. As a broad guide, many investors look for yields that remain close to:

These benchmarks help assess whether a property is priced reasonably relative to its income potential.

Access to primary schools is a major consideration for family buyers, making it one of the most reliable drivers of owner-occupier demand. Homes located within a 1km radius of schools are often preferred because this distance improves enrolment priority and offers daily convenience for parents and children alike.

Projects near multiple established schools tend to attract stronger resale interest from families planning ahead for Primary 1 registration. Even though there is no official ranking of “top schools,” parents frequently exchange views on school reputations through community networks and online forums, shaping real buying behaviour on the ground.

For many households, school proximity is not just about prestige but about practical lifestyle benefits. Shorter travel time reduces transportation costs, allows children to commute independently at an earlier age, and better aligns with working parents’ schedules. These everyday advantages create a steady pool of genuine buyers regardless of broader market cycles.

From a long-term perspective, locations close to schools often show:

For these reasons, the school factor remains a meaningful factor when assessing a property’s resilience and future appeal.

WhatsApp us

Share what you’re considering. I’ll reply with a data-backed view and what to watch out for.

By submitting, you agree to be contacted for this request. Your details won’t be shared.