15-Month HDB Wait-Out Period Removed: Why It Was Introduced, Why It Ended, and What Happens Next

The 15-month HDB wait-out period has been removed. Learn why it began in 2022, why it ended in 28 July 2026 and what it could mean for buyers and sellers.

A Complete Guide to Buy A Property in Singapore in 2026

A Complete Guide to Buy A Property in Singapore in 2026. Buying your first or investing in 2nd or subsequent properties guide.

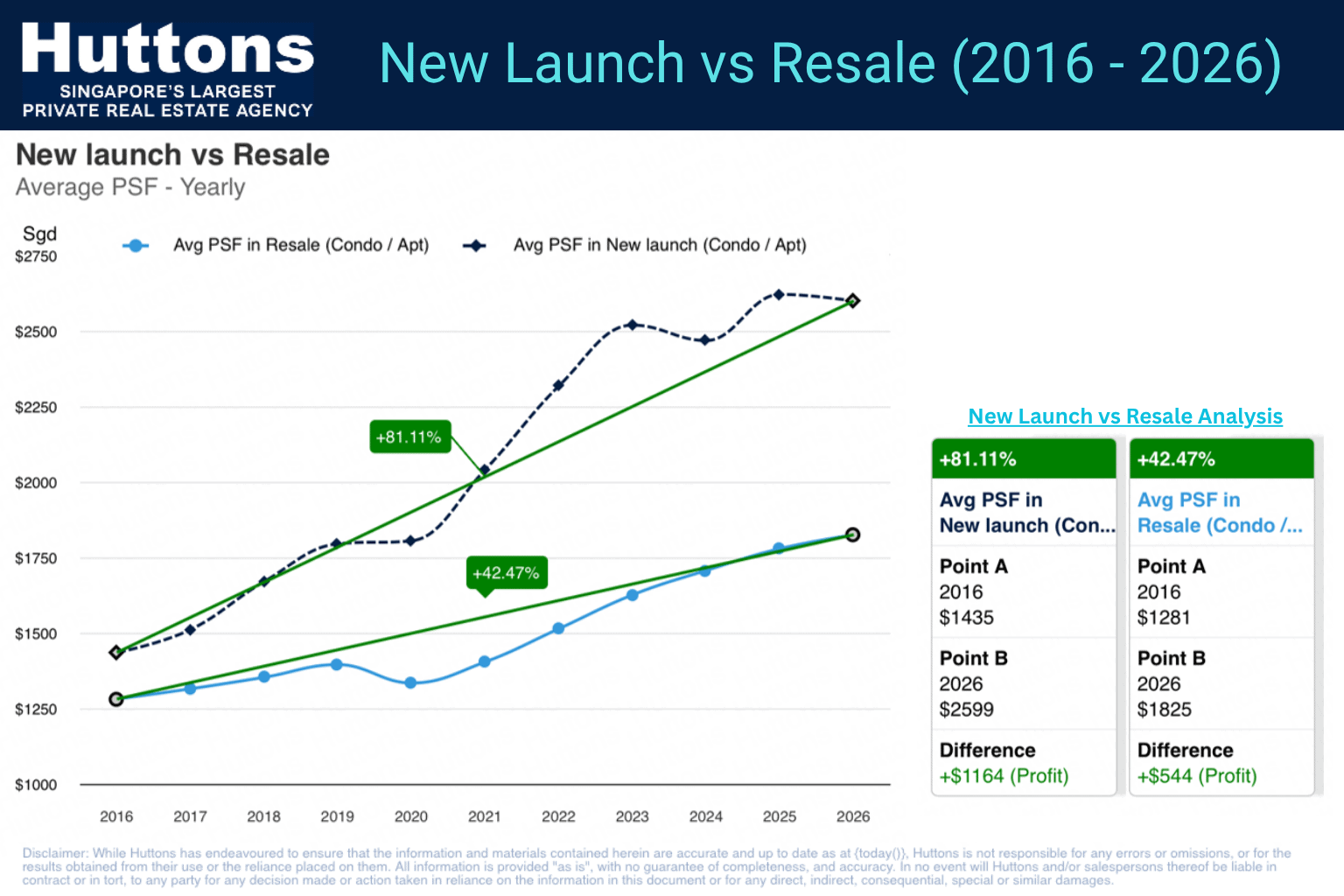

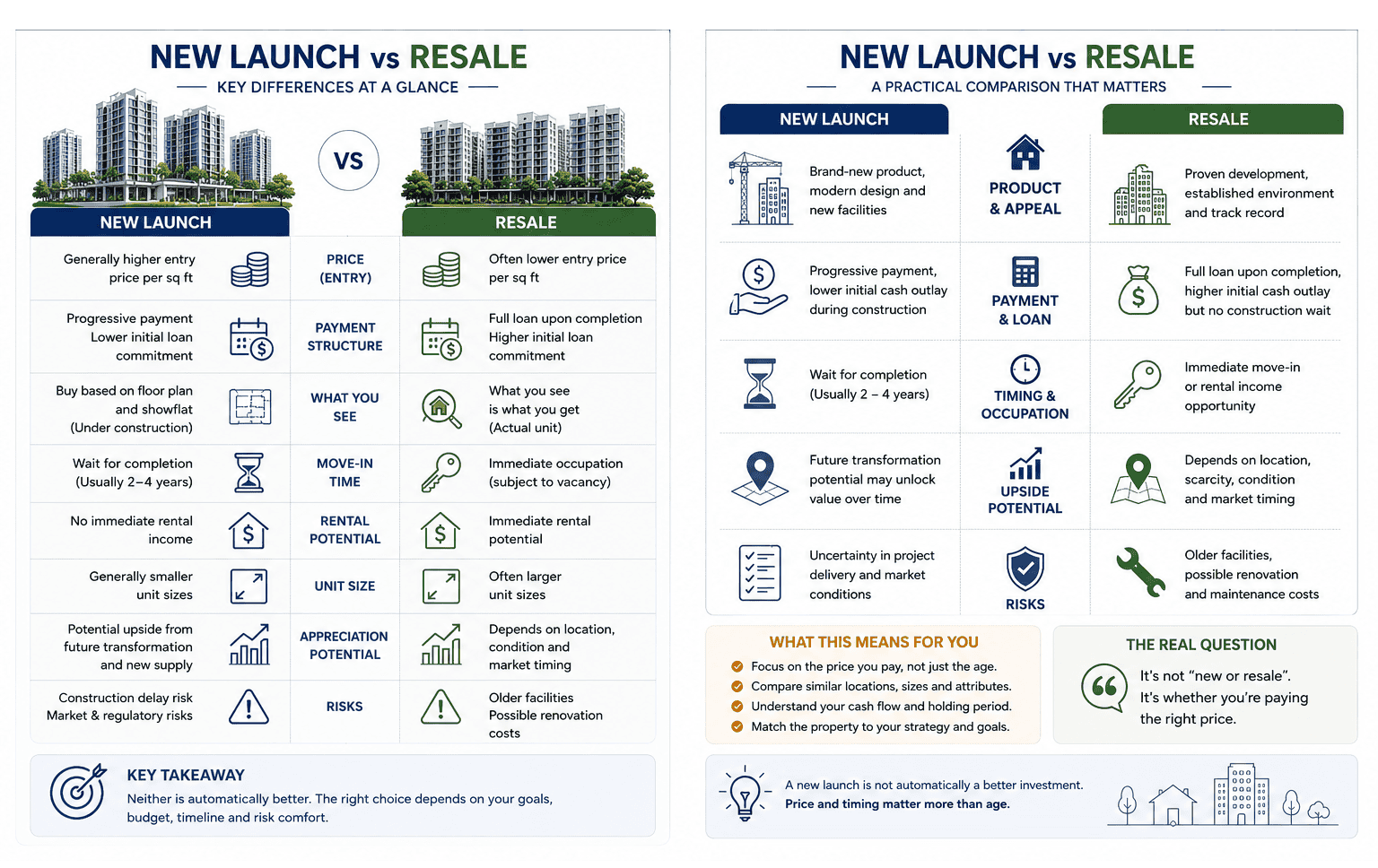

No Fluff, Just Facts: Insights Between New Launch vs. Resale Condos in Singapore

Discerning the strategic pros & cons of new launches vs. resale condos is pivotal for a fruitful property investment in Singapore.

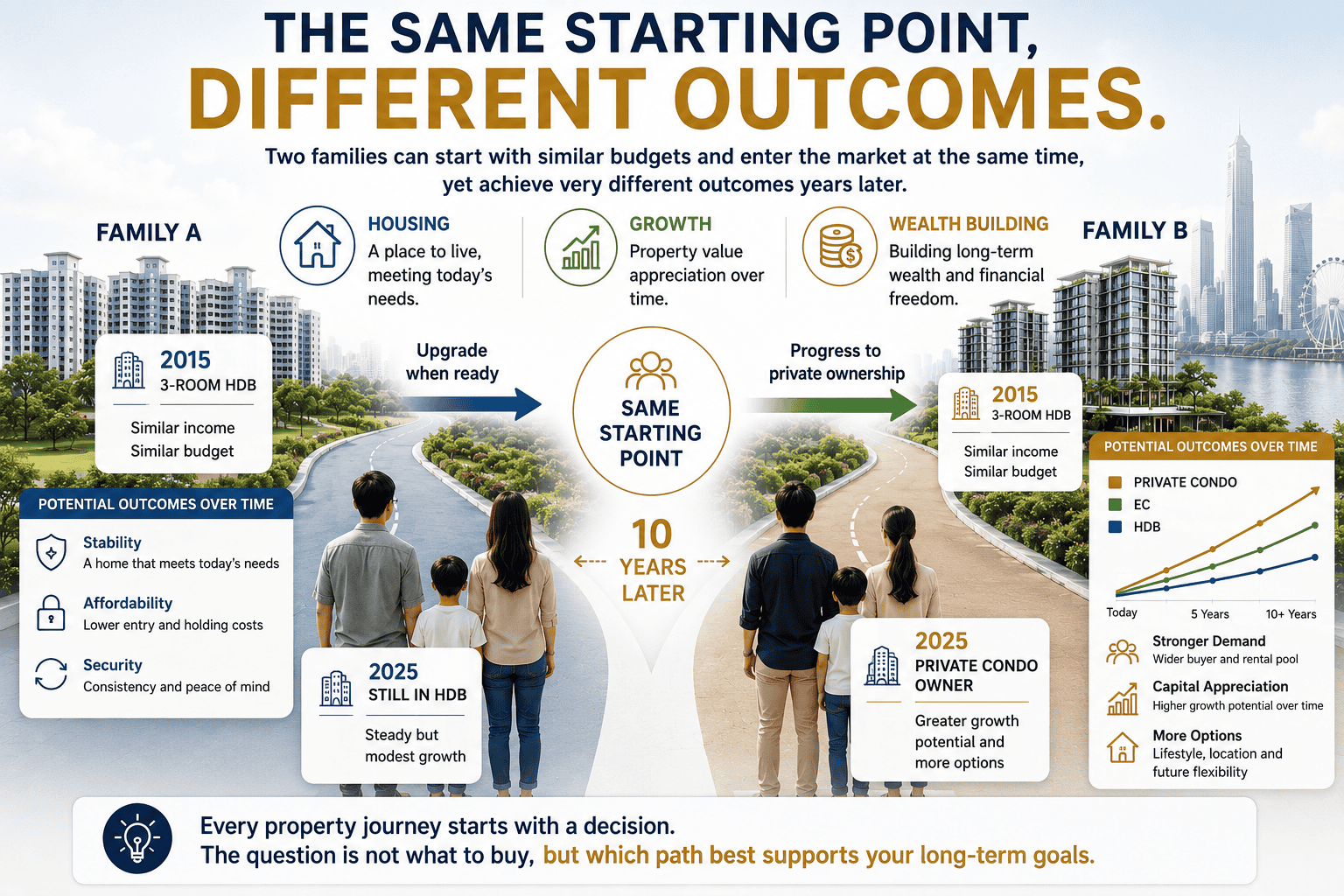

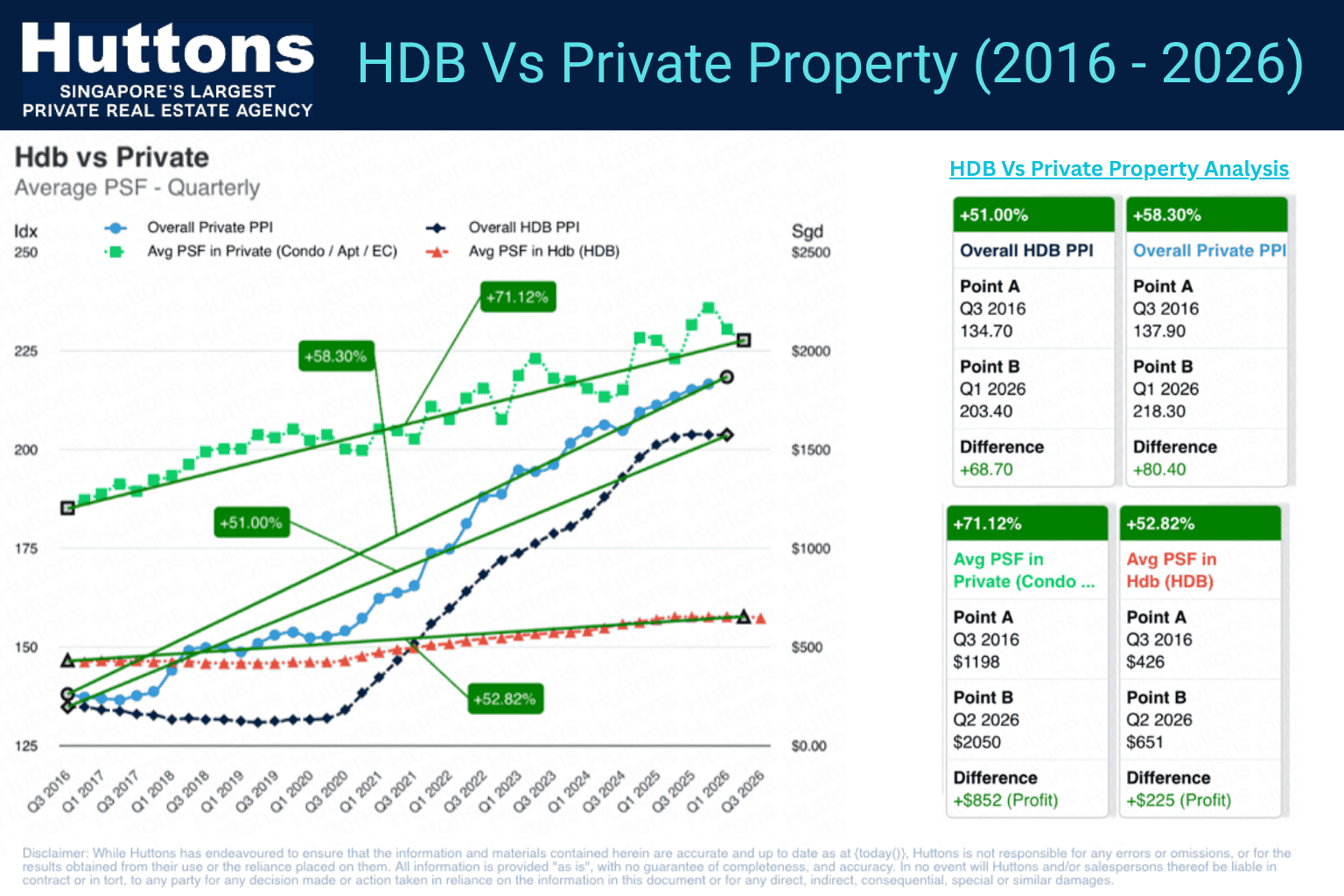

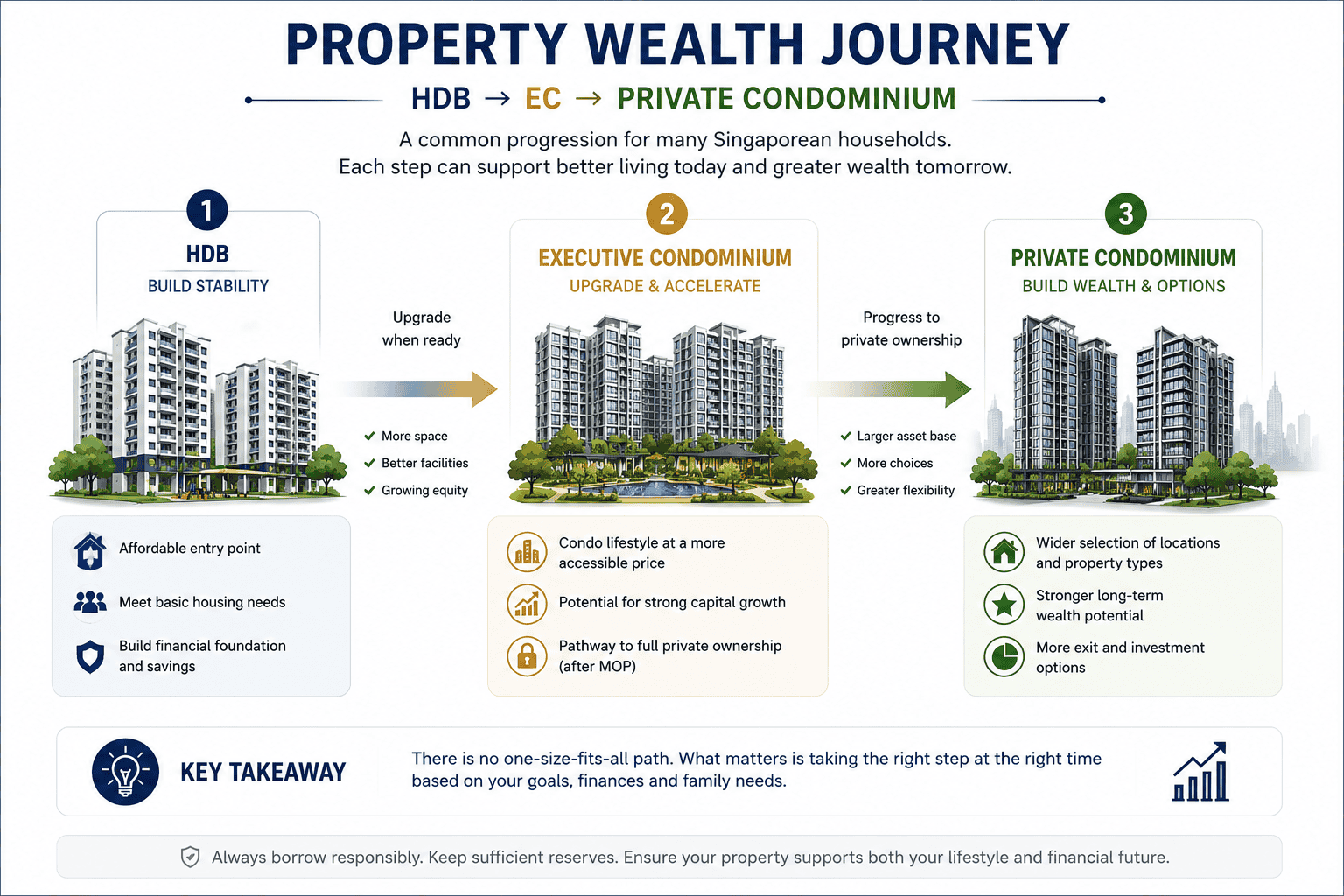

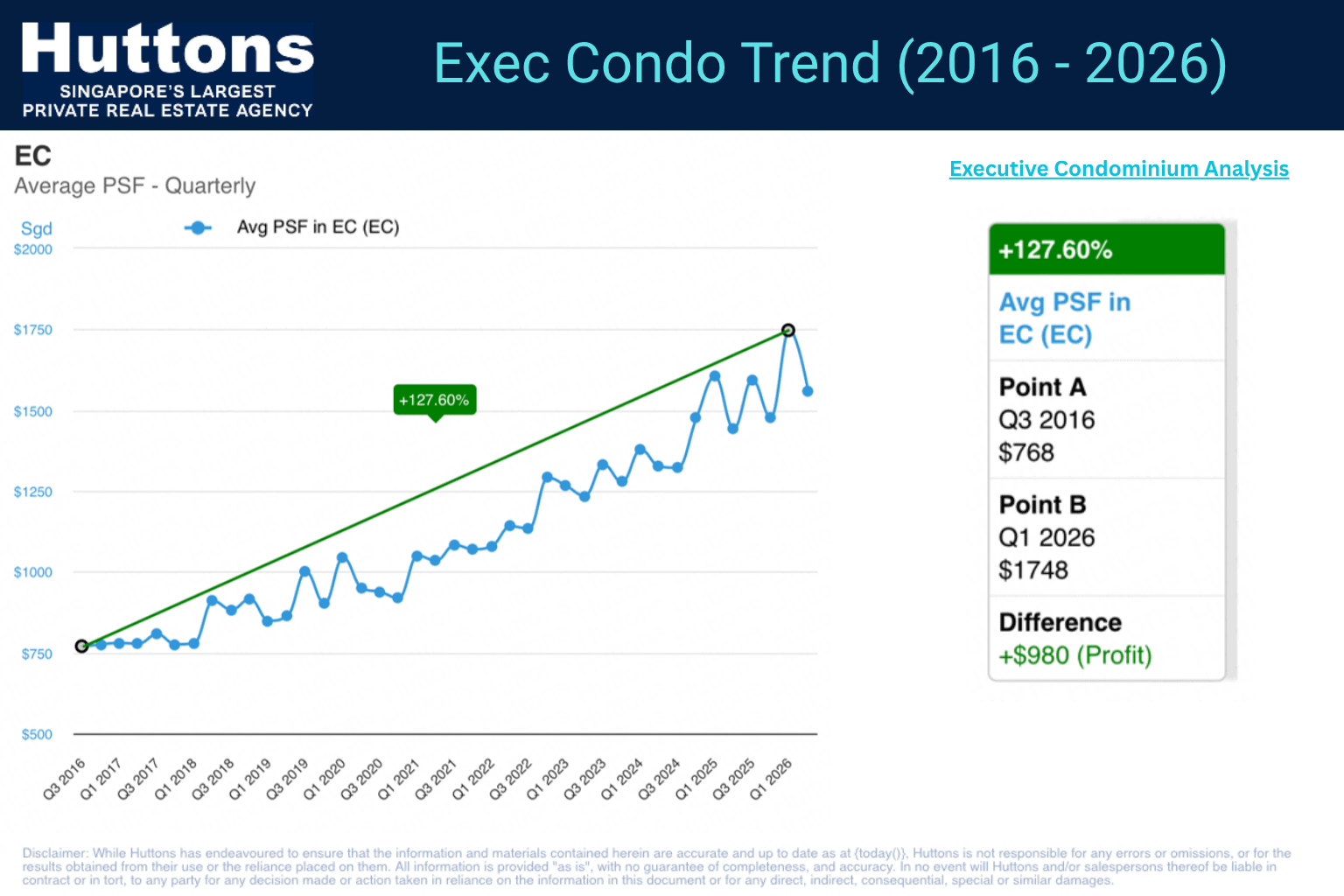

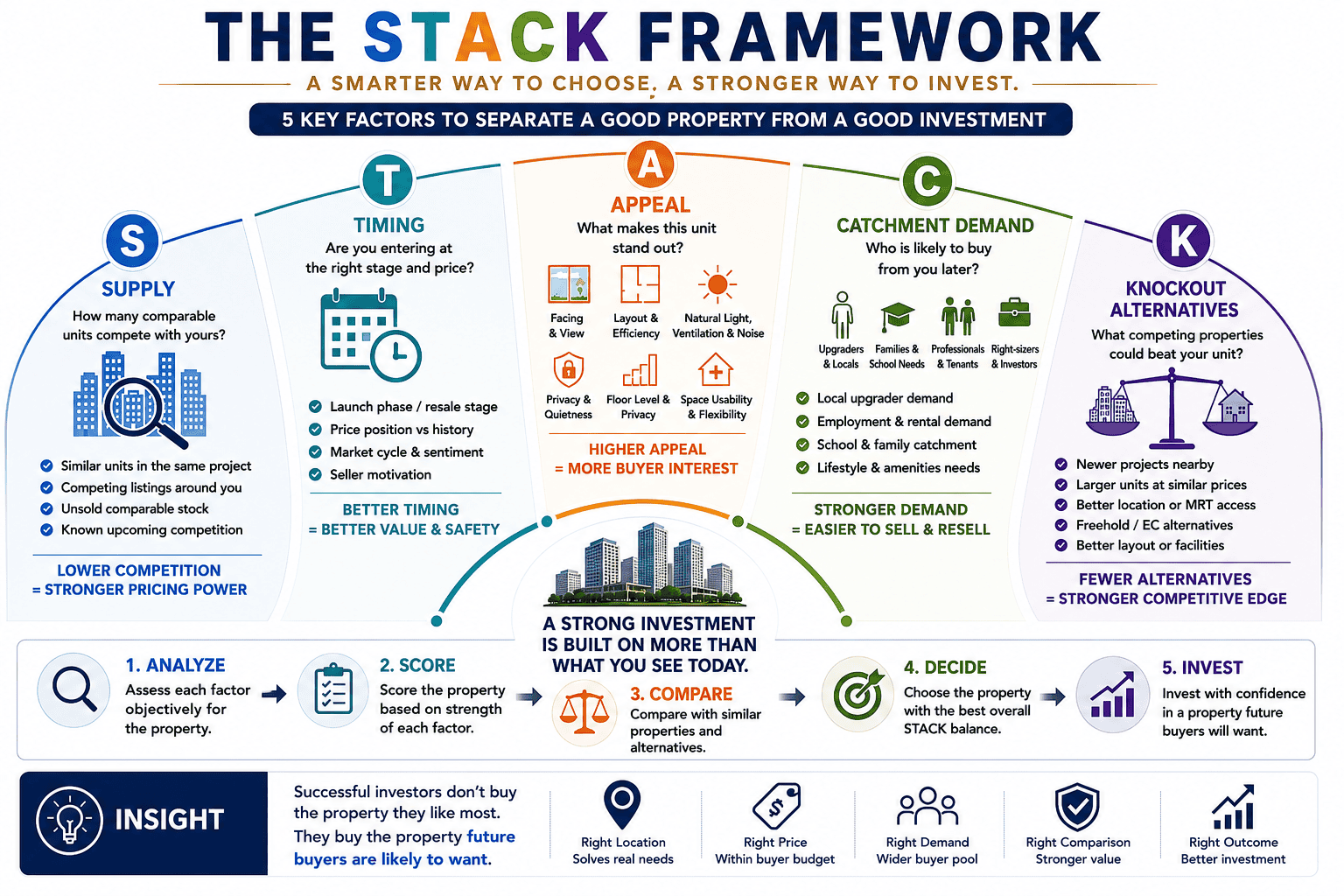

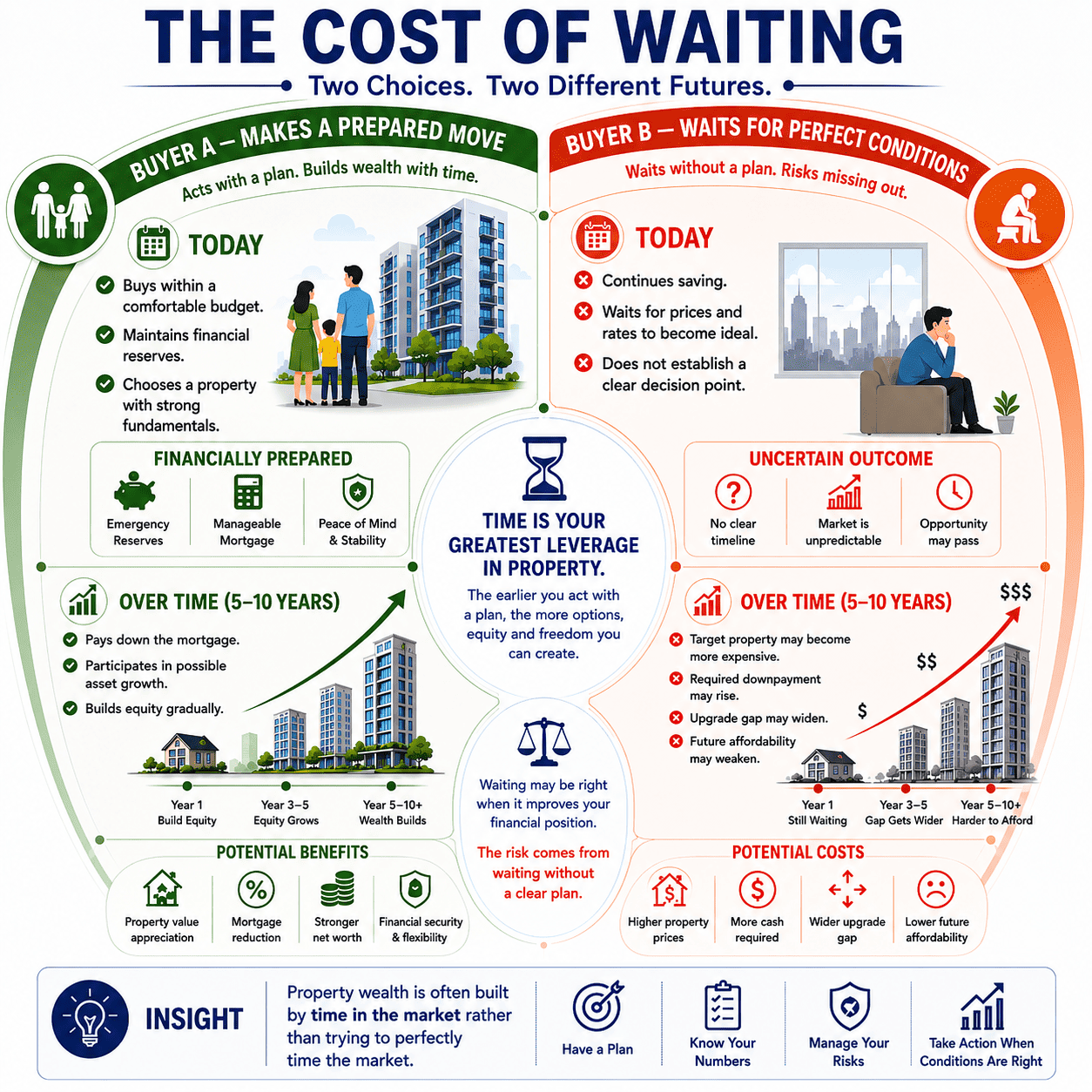

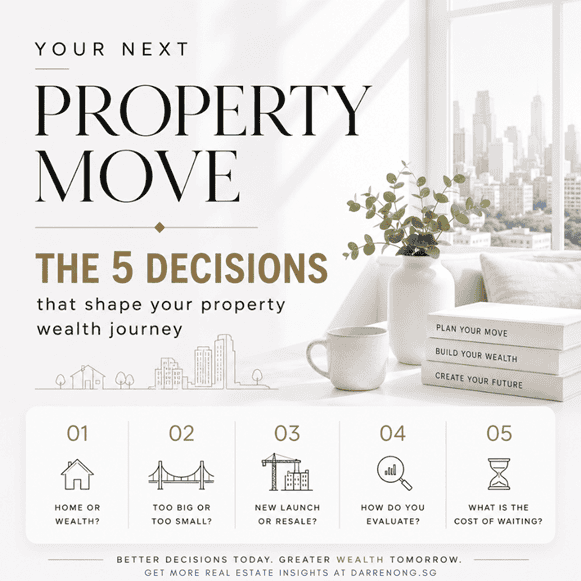

Your Next Property Move: The 5 Decisions That Shape Your Property Wealth Journey in Singapore

Table of Contents Your Next Property Move: The 5 Decisions That Shape Your Property Wealth Journey in Singapore Property decisions rarely begin with numbers alone. They often begin with a change in life: the kids need more space, the commute feels too long, an HDB owner starts wondering if their

Property Investment Insights: Comprehensive Guide to Singapore Districts 01- District 28

New Launch Property Investment or Looking to Buy For Own Stay. This Article Share with You About Property Investment Insights: Comprehensive Guide to Singapore Districts 01- District 28.

Property Investment Insights: Comprehensive Guide to Singapore Rest of Central Region (RCR) Districts

New Launch Property Investment or Looking to Buy For Own Stay. This Article Share with You About Property Investment Insights: Comprehensive Guide to Singapore Rest of Central Region Districts